Fact Sheets And Publications

Helping Your Child Learn To Manage Money

Money is necessary to meet needs and wants in our society and everyone needs money management skills. These skills are cultivated out of the ideas, attitudes, habits and values we acquire about money as we grow up.

Children who are given appropriate opportunities to make a spending plan and implement it are more likely than others to develop good judgment about money use and learn to accept the consequences of their decisions. They are also more likely to have confidence in their own abilities to make decisions and be self-reliant. They will have a head start on some of the more complicated tasks faced by adults - dealing with credit, taxes, insurance and investments. By giving children opportunities to learn about money management, parents help them develop into responsible, knowledgeable adults.

How Do Children Learn?

Children's readiness to learn depends on their interests, abilities, levels of understanding and needs rather than on their age. Parents who are aware of the many ways that children learn can help provide them with positive learning experiences starting at a young age.

1. Indirect teaching - observation and example. Children observe what their parents do with money and how their parents feel about it. What they see and hear influences the attitudes and values they develop. For this reason, it is important that parents evaluate their attitudes about and practices with money. Do you endeavor to meet financial commitments? Are you calm and rational about money matters, or is money a source of conflict and emotional outbursts? Is your spending based on whims or on a spending plan?

{kind=link}

2. Participation - taking part in discussions and decision-making. Parents can help children understand money matters by including them in regular family discussions so that they begin to know what the family income is used for and what the family's long- and short-term financial goals are. Children who understand the financial situation are less likely than others to make unreasonable demands for money. It is important to set ground rules for these family sessions so that you both know in what ways your child is expected to participate. You can stress the importance of confidentiality.

3. Direct teaching and planned experiences. At times you will want to plan an experience or situation that provides you the opportunity to teach a special lesson. For example, while playing "store" with your 7-year-old, you can point out the difference in value between a nickel and a dime. You may take your child to the library to help find and read together the Consumer Reports article on buying a bicycle. Remember that your child will likely learn more from a pleasant interaction between the two of you and from some real experiences rather than making decisions from your lectures.

4. Opportunities for making choices - real decisions. We all "learn to do by doing". Children learn a lot when parents give them the opportunity to make choices about money use that are appropriate to their stage of maturity. It's true they will sometimes make poor choices. These are times when parents can provide guidance and support, keeping the lines of communication open, rather than ridiculing or criticizing.

{kind=link}

What Should A Child Learn?

1. Money limits and choice making. A child (along with the rest of us) must learn that money is limited but wants seem to be endless. Because money is limited, we all have to make choices about how to allocate it to receive the most satisfaction possible. You can help your child learn:

- To live within money limitations.

- To learn to make adjustments when money becomes scarce. - To live with the consequences of decisions.

This will give your child a head start on successful living.

2. Opportunity costs, setting priorities. Choices are important because, once money is spent for one thing, it cannot be spent for another attractive alternative; so there are lost opportunities. Therefore, it is important to spend money on the most important things first. Through the process of evaluating which wants his/her limited money should satisfy first, a child:

- Learns to prioritize wants.

- Learns to differentiate between what is important and what is not so important. - Recognizes that needs and wants are different.

You can share with your child how you make your choices based on the values and goals that underlie your decisions. It is important for a child to have opportunities to make choices with parents' guidance and support. Choices that work out well give you the chance to offer praise and share in your child's pleasure. Of course, some choices will not be wise. At these times, you can help assess what went wrong and provide encouragement for future decision-making.

3. Conservation and dollar "stretching". A child can learn that limited amounts of money can satisfy more wants if he/she takes care of the things he/she already owns. Money spent to replace misplaced or misused toys or clothing cannot be spent on new and desirable alternatives.

{kind=link}

In addition, you can find numerous opportunities to help your child learn the benefits of becoming a good "world citizen" (through example and discussion) by conserving scarce resources and avoiding waste. For example, walking to a nearby store rather than driving has positive effect on the environment as well as on your checkbook. Not using the car reduces air pollution, conserves gasoline and reduces transportation expenses.

You can help your child learn that appropriately substituting time and skills for spending "stretches" available money. For example, replacing buttons on a shirt or hemming a skirt means the clothing does not have to be replaced. Thus, the replacement dollars are freed for other desirable choices. In addition, it gives you opportunities to teach everyday living skills that will be useful throughout your child's life.

It is important for a child to know that buying is not necessary to satisfy every want. Learning to be creative can be rewarding. Making a friend's birthday card or designing a Halloween costume from other family members' discarded clothes stimulates creativity. It also helps a child become aware of the usefulness of available resources.

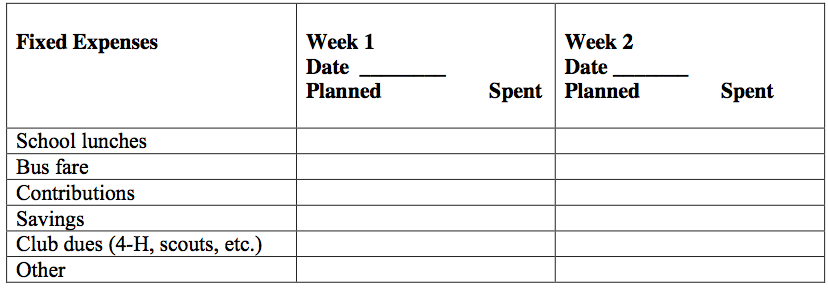

4. Setting goals and making money plans. When a child is old enough to depend on receiving an allowance (usually sometime between 7 and 9 years old), it is time to help develop a money plan. The plan should be a simple one that your child understands and should support the goals on which you both agree. Setting goals and making plans with your child can help you decide what an allowance should be. For example, if your child buys school lunches, belongs to 4-H or scouting organizations, attends church regularly, the two of you can agree on a reasonable amount for these "fixed expenses". (Fixed expenses are ones that are predictable and occur regularly.) Your discussion also gives you an opportunity to explain how spending money on these activities fits in with your values and goals.

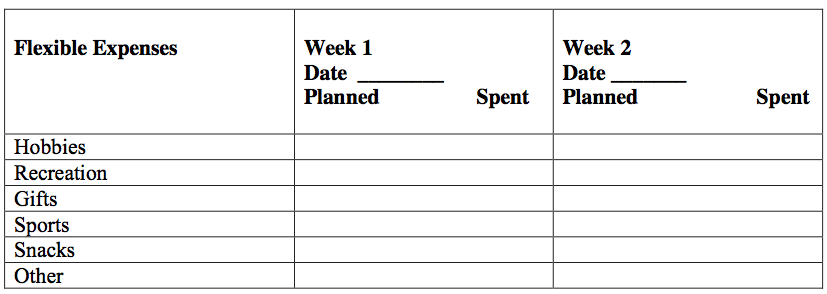

In addition, you will probably want to decide on a regular amount for flexible expenses - less essential but desirable items such as recreation, snacks and hobby expenditures - which give your child experience in making choices and living within a budget. The amount of money involved and the degree of independence allowed in decision-making should depend on your child's maturity and experience.

This is a good time to teach about setting aside a small amount for emergency funds. Your child can learn the importance of always having money on hand for an emergency phone call or bus fare home.

5. Saving and sharing. It is important for a child to learn how to make plans for sharing and saving as well as for buying. Planning to save for holiday and birthday presents, to share with others less fortunate, and to save for items too expensive for one week's allowance helps a child develop important habits for the future.

The idea of saving will first occur when an allowance will not cover an item your child wants to buy. To purchase it, saving the discretionary part of the allowance for two or three weeks will be necessary. You can help your child learn to implement savings plans by furnishing a container or envelope to hold the money until the desired amount is accumulated.

You can help an older child implement longer-term savings plans by helping him/her open a savings account at your financial institution. Also help your child learn how to make regular deposits in person or by mail.

6. Consumer skills. Developing good buying skills is a lifelong venture, starting with the child of 4 who learns that the candy at the store cannot be eaten until it's paid for. Important skills that your children can first observe you practicing even before being given their own opportunities in decision-making include:

7. Comparison shopping. Finding the appropriate quality at the best price is an important skill. You can start teaching this skill as you explain to your 7- or 8-year-old why you choose one item rather than another in the grocery store.

{kind=link}

8. Seeking good information. As your child matures, encourage the use of information about price and quality before making important purchases. This could include visiting several stores, using the newspaper, telephone and catalogs, as well as reading product evaluations in magazines.

- Reading labels.

- Knowing about product warranties.

- Handling returns of unsatisfactory products.

9. Borrowing. That borrowing today reduces the amount of future income available for spending is an important concept. If you decide to become a lender to your child, it's wise to keep the amount borrowed small so that repayment does not become frustrating. Insist on a repayment schedule and stick to it.

By the age of 10 or 11, your child can understand the idea that lenders charge interest, thus increasing the amount to be repaid. Learning to calculate interest costs and being required to pay you those charges introduces a child to the real costs of credit.

Sources of Income:

Gifts

Small amounts of money received as cash gifts on birthdays and holidays can be used, as the child desires. The major portion of larger gifts can be invested in some form of savings to provide for future use. This gives your child the opportunity to establish long- term goals and the means to begin implementation.

Rewards

Money is sometimes given to children to reward them for good grades or good behavior. It may actually serve as a bribe, sending the message that good behavior has a price. It is best to keep money out of situations that do not involve its use. Praise, smiles and hugs are good ways to encourage good behavior and good grades.

Allowances

An allowance is a certain amount of money given to a child on a regular basis. It's a good tool to begin to teach children the basics of money management. Sometime during the early grade school years, between ages 7 and 9, children can begin to handle regular sums of money to cover their expenses for a few days. The allowance will cover items a parent pays for anyway (school lunches, activities, treats), so you won't necessarily be spending more money.

The purpose of an allowance is to begin to shift some of the responsibility of goal setting, planning, implementing and decision making from you to your child.

How much?

Three factors will determine the appropriate amounts: the amount you can afford, the child's level of maturity and the items the allowance will cover.

The allowance must fit into your budget, not be based on what

the child's friends receive or what your child wants to have.

As your child matures and his/her responsibilities at school and in the community increase, the allowance should increase so that larger sums of money cover longer planning periods. In the beginning, a short planning period of two or three days might be appropriate. Later on, an allowance might become weekly.

What activities and functions is the allowance supposed to cover?

To avoid conflicts and to ensure that your child can successfully manage the allowance, it is vital that you both understand the answer to this question. Remember, too, that as your child develops, increased responsibilities at school and in the community will call for larger allowances.

Allowances should provide for more than necessities (school lunch and bus fare). If your child is to gain valuable experience in decision making and learning about money limits, some extra money for spending or saving is needed. Together you can decide the amount that fits into your budget. Don't forget that this extra money gives your grade schooler experience in setting priorities and making choices.

What an allowance is not

An allowance is not pay for routine work at home - it is an opportunity to learn money management skills. If it becomes a reward for accomplishing some routine tasks such as bed making and table setting, then when the chores are not done, you may feel forced to withhold the allowance. Receiving an allowance then becomes an emotional issue between the two of you, rather than an opportunity for gaining money management experiences.

As a member of your family, your child has rights (such as access to some of the family money) and responsibilities (such as helping to keep the house tidy). If the child shirks some of these responsibilities, it is best to handle this as an issue separate from the allowance. Remember, too, the importance of showing your appreciation for help with the regular family chores.

Earnings for Extra Work at Home

Sometimes parents hire their children for special household jobs that are done only occasionally, such as cleaning the garage or washing the storm windows. The pay supplements the child's allowance and having the jobs done helps the parents.

It is important to work out in advance how the pay will be determined and what your expectations are. Keep it businesslike. As you would with anyone you hire, be sure the correct tools are available. Remember that training may be necessary to increase the chances of a job well done. Once hired, your child becomes a wage earner like anyone else you might hire. Will it become an emotional issue between you if the child decides to quit because he/she dislikes the job?

Earnings for Extra Work at Home

Sometimes parents hire their children for special household jobs that are done only occasionally, such as cleaning the garage or washing the storm windows. The pay supplements the child's allowance and having the jobs done helps the parents.

It is important to work out in advance how the pay will be determined and what your expectations are. Keep it businesslike. As you would with anyone you hire, be sure the correct tools are available. Remember that training may be necessary to increase the chances of a job well done. Once hired, your child becomes a wage earner like anyone else you might hire. Will it become an emotional issue between you if the child decides to quit because he/she dislikes the job?

Handout or doles

Some parents seem to prefer handing out money as their children need it. This method doesn't help a child learn to plan. How much money and when it will be available are never definite. Children often become adept at begging and manipulating parents to get as much money as possible.

It becomes a great bother to parents to have to make decisions every time a child asks for money. Additionally, it becomes difficult for the parents to keep track of how much is being spent. Doling out money upon demand is not a recommended method for teaching money management.

What about special occasions?

Of course, special occasions will arise that call for money beyond the limits of the allowance and earnings. Even if you have set an appropriate allowance, make it clear that special money needs will be discussed as they arise. This gives you the opportunity to decide with your child it this special occasion will provide something that has long-term benefits and to determine if it fits into your budget. If it does fit into your budget, you may decide to supplement the allowance this time.

Providing a loan to your child is also a possibility, but the loan should be limited to an amount that the child can readily repay from his/her allowance or earnings within a few weeks. The load will require both of you to agree on a repayment schedule. Writing the payment dates on a calendar will serve as a reminder.

{kind=link}

If it doesn't fit into your budget, explain your financial situation and provide support and understanding as your child learns that money availability has limits.

If these "special occasions" seem to be arising often, it is time to review the situation with your child. Either the amount available from the family income is too small, or wants are out of line (or a combination of the two is occurring).

Together you can analyze the problem to find a solution. Maybe the “wants” need to be more realistic, and you can help in setting priorities. Maybe the allowance has not increased appropriately to match your child's maturity, new interests and responsibilities. Maybe the family budget is stretched to its limits, and a part-time job is needed to supplement the allowance.

Earnings from Jobs Outside the Home

Working outside the home is an option that you and your older child or teenager may decide is appropriate. The pay will help to supplement the child's allowance, provide for ever-expanding wants and perhaps provide some financial relief to parents.

Employment also fosters an understanding of the relationship between money and time, skills and effort. Working and earning can help enhance the self- esteem of young people as they discover that they have abilities for which someone is willing to pay.

By the age of 9 or 10 years, your child can earn money from occasional jobs for neighbors or friends such as leaf raking, yard mowing and babysitting. These activities may last for several years as a child progresses through middle school.

{kind=link}

Your teenager may want to work summers or weekends at regular part-time

jobs that provide steady sources of income. Fast-food restaurants, other retail

stores and summer camps are traditional sources of jobs for older teenagers. But before your teenager looks for a job - whether it's a traditional or non-traditional one - you will want to be sure that working supports important goals you both have. Some teenagers work so much that they do not have time to keep up with their schoolwork, and they are so tired they have trouble staying awake at school.

Some important questions to consider with your teenager are:

- How many hours a week can the teen realistically work with no negative effect on schoolwork or home responsibilities? Will your teen work so many hours that he/she will take less demanding courses in school, affecting future career possibilities?

- Will the teen have time to maintain friendships and time for recreation and rest?

- How will this work restrict the activities of the rest of the family? Because an outside job will affect the whole family, everyone needs to have an understanding of what may be involved. Will it involve eating at odd hours, use of the family car, someone else taking over part of the child's family chores? What other inconveniences will be involved?

- Will the job interfere with the family's weekend and vacation plans?

You can often head off possible problems by discussing them ahead of time.

If you agree that an outside job would be a positive learning experience, you need to consider two money management issues together:

- What will your child do with the earnings?

- How will these new earnings affect the allowance you have been providing?

Teenagers can earn considerable sums of money from part-time jobs. If these earnings are all used to buy discretionary purchases, youngsters acquire an artificially high level of living that they cannot maintain once they leave home. Once independent, they will have to pay for their own necessities, such as food and housing expenses. To avoid the formation of unrealistic living standards, you can help establish some long-term saving goals for part of these earnings. Goals such as saving for college or vocational school or a first car are appropriate. Be sure to help implement these goals by helping your teen make regular savings deposits.

By working, your teenager will learn firsthand about "real world" expenses. Having a job nearly always entails some expenses that the teen will need to pay out of earnings - uniforms or other special clothing, lunches, transportation expenses, Social Security taxes. If the job entails being driven to and from work or using a family car, this is a good time to let the teenager share in some of the expenses of driving and maintaining a car.

{kind=link}

This may also be the time that the two of you decide to shift some of the financial burden of recreation and clothing expenses from you to your teenager. Over a period of time, working can give teenagers the opportunity to assume responsibility for their upkeep, to assume some independence and to learn firsthand about the high costs of living.

Helping Your Child Develop As A Money Manager

Children mature at different rates. It will be frustrating for both of you if you try to teach concepts or skills too early. The following section will suggest some experiences to help children of various ages learn important concepts and begin to develop good habits. (Remember, though, that some children will be ready sooner and some later.)

Once you start thinking about it, you will be able to add many other learning activities to the list.

This chart can be used as a guide in helping children develop a spending plan for their allowances.

Totals

Adding the totals over a period of a few weeks will give you both an idea of what adjustments need to be made in either the spending or the allowance amount.

As your child matures, the budget categories and their amounts will change. Together you can review the spending plan regularly.

Additional Sources for Parents:

Children and Money Management. Money Management Institute, Household International, Inc., 2700 Sanders Road, Prospect Heights, IL 60070. Fee.

Hughes, Theodore E., and David Klein. The Parent's Survival Guide. Tucson, Ariz: The Body Press, 1987.

Rowland, Mary. "Teaching Your Kids About Money." Money, March 1990, pp. 126-135.

Resources for Kids:

Schmitt, Lois. A Young Consumer's Guide to S-M-A-R-T Spending. New York: Charles Scribner, 1989.

Zillions, Bi-monthly Consumer Report's magazine for kids age 8 - 14. Zillion’s Subscription Department, P.O. Box 51777, Boulder, CO 80321-1777.

Estess, Patricia Schiff and Irving Barocas. “Kids, Money & Values – Creative Ways to Teach Your Kids About Money”. Betterway Books, 1994.

Written by Rosemary Walker, Associate Professor and Irene Hathaway, Extension Specialist Department of Family and Child Ecology Michigan State University.

Adapted for Delaware Cooperative Extension by Maria Pippidis, Extension Educator, Family and Consumer Sciences. For more information contact your local Extension Office.

UD Cooperative Extension

This institution is an equal opportunity provider.

In accordance with Federal law and U.S. Department of Agriculture policy, Cooperative Extension is prohibited from discriminating on the basis of race, color, national origin, sex, age, or disability.